You would be forgiven for thinking this an odd title given current macro, market and trading conditions but in our case at True, it’s very much the case. At the end of last year we spoke of our internal caution highlighting significant supply and demand pressures resulting in major market dislocations in which the reality of current trading was not reflected by stock market expectations.

Since mid-December, this reality has begun to bite investors, a process which was underway well in advance of the tragic events unfolding in Ukraine. Back then we referenced Allbirds’ stratospheric valuation (now down 80% in the last 12 months and 63% since the start of January) but that scale of decline isn’t limited to overpriced US IPOs. On our own shores, Seraphine (-76% since IPO) and Boohoo (-45% YTD, -79% over 1 year) all point to a market reflecting a significant shift in outlook and a material reassessment of prospects.

This dynamic is especially profound in companies that are not generating cash and don’t have evidence of sustainable economics. Whilst many have not yet reached valuation levels that are commensurate with the level of risk, the direction of travel is clear, and opportunities will arise as fear overwhelms greed in markets. This is the time when bravery and a long-term view will be handsomely rewarded as markets adjust to newly apparent realities.

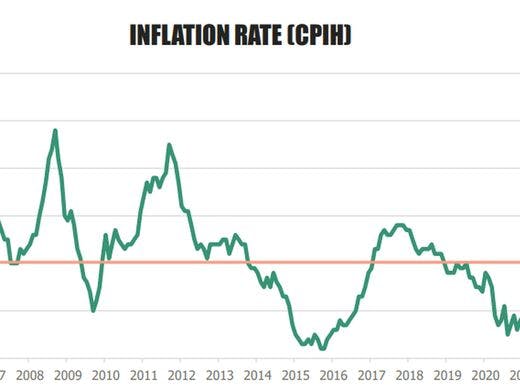

This need for bravery flies in the face of all macro indicators. Consumer confidence has fallen sharply towards the levels last seen in March 2020 at the advent of the first Covid lockdown. This confidence is being eroded, as forecast, by inflation where the media lose no opportunity to remind consumers that their household budgets are rising.

Inflation is beginning to permeate all aspects of daily life, even those where the value proposition has noticeably weakened over time. Income available for discretionary spending will erode further as food, petrol and utility bills continue to mount.

Yet, despite these pressures, the labour market is incredibly strong. Unemployment is low by any historical measure and vacancies are at all-time highs. There is currently only one unemployed person per job vacancy, a record low, vs. a long-term average of 3. The unit cost of labour is rising and, given demand pressures, it feels a matter of time before companies become more proactive in managing costs.

What does this mean? In short, companies face a very difficult period of steep cost inflation across the entire P&L whilst also competing for customers with falling confidence, their own cost pressures and, accordingly, less inclination to spend. Some categories, such as apparel, are even deflationary currently as brands seek to reduce stock overhangs, further weakening margins. Those without strong brand positioning will have to promote to drive new and repeat customer acquisition whilst already facing high (and also rapidly rising) digital marketing costs.

Central banks have been blindsided by inflation and the risk of policy missteps has increased dramatically since the turn of the year. A hard landing for the economy is a real prospect. This will bring asset prices down, potentially sharply as markets are prone to over-correction.

So what can be done? Firstly, in this environment companies need to innovate which requires investment and is therefore counter-intuitive in tough market conditions. Think of it as “training at altitude”. Secondly, as accelerated corporate Darwinism (largely on ice since 2008/2009) re-emerges, many players will get into difficulties, market share opportunities will arise and the supply and demand imbalances will reset.

At times like this, it is tempting to become insular and ignore bigger opportunities and the power of compounding economics. Technology still grows exponentially, derivations of Moore’s law persist and it is worth paying attention. At the intersection of consumer behavioural change and technological development, sizable new markets are being formed. For example, prize money in E-Sports, reflecting the commercial potency of its core audience, has increased from $177k to $728m since 1998 – growth of 4,000x. Meanwhile viewing figures for the Olympics have fallen by 55% since 2018. Not all fads become secular trends, of course, and not all emerging industries deliver profitable outcomes but times of economic dislocation have always spawned disproportionate opportunities.

True is open for business, and so should you be.